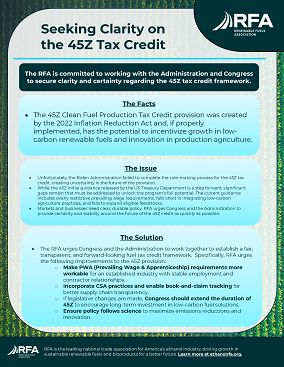

To encourage the continued growth and expansion of renewable fuels like ethanol, federal and state governments offer financial incentives to help drive innovation in the industry and to make ethanol more accessible to American consumers. However, to be truly effective, federal renewable fuel tax policy must be reformed in a way that creates a consistent and stable tax policy framework for ethanol producers and industry investors.

RFA is also working to expand the incentives available to the industry so they recognize changing market dynamics and ongoing consumer and industry challenges. That’s why the RFA is working together with policymakers to improve current renewable fuel tax policy, making it more effective at driving growth and innovation in the industry.

RFA is committed to finding long-term solutions that enhance the existing suite of tax incentives while properly deploying new programs.

RFA Tax News Releases RFA 45Z News Releases