By Geoff Cooper, RFA President and CEO

Earlier this week, I had the honor of testifying before a House Energy & Commerce Committee subcommittee on the devastating impact of small refinery exemptions (SREs) on the U.S. ethanol industry.

My testimony described the demand destruction that has occurred as a consequence of the massive increase in SREs. I told the subcommittee that EPA's mismanagement of the SRE program has "...rendered EPA's annual Renewable Volume Obligation rule meaningless, introduced tremendous uncertainty into the marketplace, and significantly undermined demand for renewable fuels." The testimony pointed out that SREs have led to the temporary idling or permanent closure of at least 19 ethanol plants since spring 2018.

Not surprisingly, testimony from the American Fuel & Petrochemical Manufacturers attempted to paint a much different picture. AFPM claimed everything is just fine in the ethanol industry and asserted that SREs are not eroding domestic demand for ethanol. Tell that to the 700 ethanol plant workers who have been laid off or furloughed because of deteriorating conditions in the ethanol market.

While I refuted many of AFPM's claims during the question-and-answer segment of the hearing, I unfortunately did not have the time to address some of their most egregious arguments. So, let's do that now.

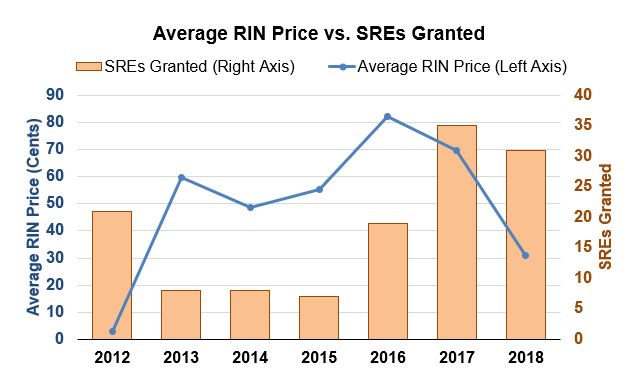

The Claim: AFPM suggested the four-fold increase in SREs in recent years was due to higher RIN prices, stating, "Rising RIN and compliance costs of the RFS is what explains the rise in SREs in recent years."

The Facts: The surge in SREs has had nothing to do with RIN prices.

RIN prices hit a six-year low in 2018, but EPA handed out 31 SREs anyway (the second-most ever). In fact, average RIN prices were much higher in 2013-2015, when only seven or eight SREs were granted annually, than in 2018. RIN prices averaged 55 cents in 2013-2015 when a total of 23 SREs were granted; and averaged 61 cents in 2016-2018 when a total of 85 SREs were granted. How does a modest 10% increase in RIN prices justify a 270% increase in SREs granted and a 487% increase in the volume exempted!?

Meanwhile, 21 exemption extensions were given in 2012, when RIN prices averaged just 3 cents. Clearly, there is no relationship between RIN prices and the number and size of SREs granted. And if "high RIN prices" are the justification for SREs, as AFPM stated at the hearing, then we should not see any SREs granted for the 2019 compliance year—because we had the lowest RIN prices in seven years!

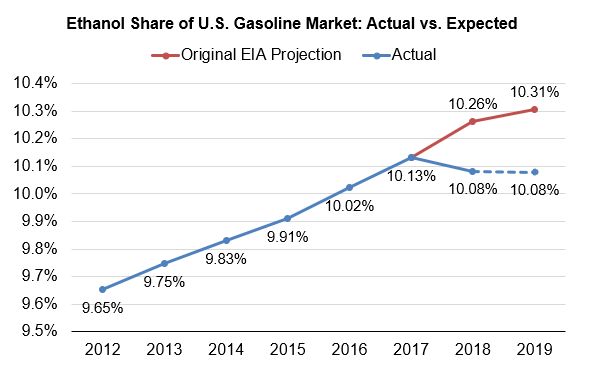

The Claim: "The notion that SREs are hurting biofuels market share is false."

The Facts: Ethanol's market share has fallen since the surge in SREs.

By definition, "market share" refers to the portion of a market's total sales that is comprised by a particular product relative to competing products. In 2017, ethanol's share of the gasoline market hit a record 10.13%, slightly above the so-called "blend wall."

In January 2018, EIA forecast that ethanol's share of the gasoline pool would continue to grow, driven by the RFS. EIA expected ethanol's market share would increase to 10.26% in 2018 and 10.31% in 2019.

However, once the marketplace became aware of the massive increase in SREs in the spring of 2018, domestic ethanol blending began to drop, as refiners opted to comply with marginal RFS requirements using a deluge of cheap paper credits (RINs) in lieu of expanded ethanol blending. In fact, ethanol's market share fell to a three-year low of 9.67% in April 2018.

For the full 2018 calendar year, ethanol comprised 10.08% of the gasoline pool—the first annual decrease since at least 2009. And now, with just two months left in 2019, EIA expects ethanol's market share will be stagnant at 10.08%, compared to the original expectation of 10.31%. The difference may seem trivial, but it's not. Across 143 billion gallons of gasoline, even a 0.23 percentage point change in demand equates to significant volumes.

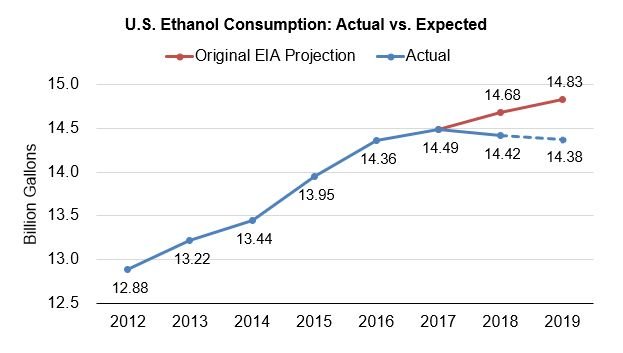

The Claim: "EIA data demonstrate consumption and blending are at or near all-time highs."

The Facts: Ethanol consumption is falling since the massive outbreak of SREs in early 2018.

Not only is ethanol's share of the gasoline pool falling in the wake of SREs, but the absolute volume of ethanol blended is decreasing as well. Domestic ethanol consumption peaked a 14.49 billion gallons in 2017, fell for the first time in 22 years in 2018, and is projected by EIA to fall again in 2019.

Actual ethanol consumption in 2018 was 260 million gallons below the level initially expected by EIA prior to the SRE bonanza, and actual 2019 blending is on track to fall 450 million gallons from the initially projected level.

So, while AFPM continues to suggest that things are going great in the ethanol market, the facts on the ground tell a much different story. We hope lawmakers and EPA regulators see through the refiners' smokescreen and take steps to get the RFS back on track.